The venture community’s reaction and next move as a result of the crisis that hit our world this year will vary depending on who you speak to. We have been told that 75% of investors have confidence in completing a full deal cycle virtually, but what sort of investors are they? And at what level of investment does this confidence start to appear or disappear?

Venture investors by category

In order to dive deeper, I will introduce you to the different types of venture investors. Venture investors come in different shapes and sizes and the lines between them have become increasingly blurred in recent years. They tend to fall into five categories:

1. VCs

Venture capitalists (for example Nauta Capital or Index Ventures) are the traditional venture investors that take minority investments in early-stage, fast growing companies. These are completed in rounds (Series A, B, C etc) in companies that will usually not be profitable, but that have a unique business offering with the potential of fast growth and the opportunity of a large future sale / exit.

Why do VC’s typically require such a high return profile?

Similar to start-ups, VCs will spend a period of time fundraising. A typical VC will spend several years fundraising from Limited Partners (LPs) to raise a fund, which is then typically invested across a three to five year period. They are handling the wealth of others with the promise of a strong financial return, and therefore a high return is required. It is this ‘gamble’ that the venture industry thrives off, but it is also what drives the high return requirements. VCs will often look for a minimum return profile of 10x (because only one or two of their investments will usually return the fund, with the majority failing to return anything).

2. VCT / EIS funds

VCT and EIS funds allow their retail investors to gain income tax relief of 30% on their investments. They have been a popular scheme for a number of years, particularly for those that have been ‘pension squeezed’ (i.e. maxed out their contribution limits) or are in upper rate tax brackets.

What is the difference between VCT and EIS and why are their return requirements smaller than VCs?

VCTs are publicly traded companies (for example Calculus VCT), meaning an investor would buy shares in that fund / plc that will then invest into a portfolio of start-ups – similar to utilising a fund manager on the stock market. On the other hand, EIS funds (for example Guinness Asset Management) will invest money on behalf of others in individual companies.

VCT and EIS funds will typically seek to invest in companies that have a return profile of 3-5x. Broadly speaking, this much lower return than traditional venture capital investors is due to the fact that the investor will immediately benefit from a 30% gain on investment due to the tax relief. The lower return is also a function of capital preservation that is often sought by VCTs and EIS funds.

3. Family Offices

Often seen as a very desirable investor group by founders, Family Offices will invest the money of one or more high net worth families. The investments can sometimes be described as ‘patient capital’, which points towards the longer term intentions of their investments, as opposed to seeing a financial return within a set period of time. Best get your networking hat on though! Family Offices are not the most accessible funds and typically do not advertise themselves across the Internet – they like to be known through smaller circles. For more information on Family Offices, please see this interview on hunting unicorns with Glen Waters, Head of PwC Raise.

4. Corporate Venture Capital (CVCs)

CVCs (for example Legal & General) are one of the newest sources of venture that have come to light over the last decade. A CVC will typically have two objectives:

- Assist in developing the strategic pathway of its parent company

- Provide an additional source of financial return for the parent company

This differs to every other investor group introduced today. Whereas all other investor groups are measured solely on financial return (or increasingly “impact” in many funds), a CVC’s performance will be measured on both strategic and financial metrics – this is something to keep in mind as we take a closer look at the data later.

5. Venture Debt

Perhaps the most ‘transactionally’ driven group of them all, venture debt (for example Boost, Shawbrook and Natwest Growth Fund) works similarly to a normal loan – money is provided (‘invested’) into your business which you then pay back plus interest over a set period of time (typically three years). Venture debt players usually come in at a growth capital stage, as they will focus solely on historical financial metrics and the forecasted expectations.

Venture debt has been described as making venture more efficient – they can be arranged much quicker than equity, although typically are invested alongside an equity provider. Venture debt funds do not generally take a board seat or require observation rights, removing independence issues on decision making.

Who out of these investor types will be the most active moving forward?

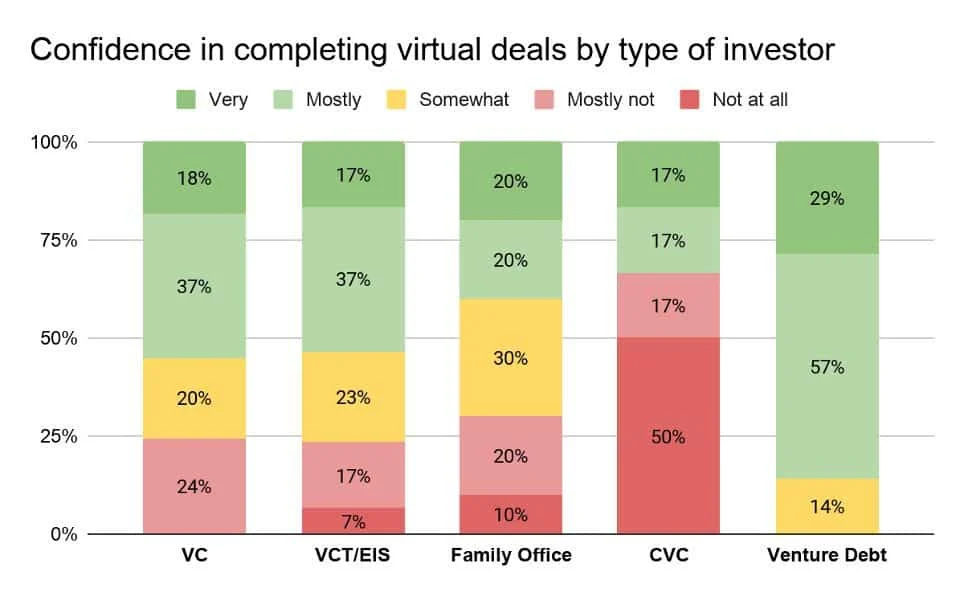

The PwC | Raise survey confirmed that almost three quarters of venture investors would have the confidence to complete a deal virtually. It’s now time to look into that analysis of 102 funds.

The more strategic the investor, the more challenging capital will be to come by

One thing that immediately jumps out through the above analysis is that CVCs are by far the least likely to be actively chasing deals during the COVID-19 period- in fact two thirds of CVCs (67% not at all or mostly not) need to get back to more face to face focused ways of investing. As we have already mentioned, CVCs are measured on two types of metric; financial and strategic. It therefore shows that the personal touch is still a high priority in deals that aren’t purely financially driven.

A CVC will often look to invest in a company before acquiring, almost to test the technological synergies before jumping into a purchase. They are therefore often working very closely with the companies they invest in on an ongoing basis. This could be looked at from the point of view of when you are hiring – few would argue that if there was a possibility of meeting individuals before they join your business full time, they wouldn’t want to do so.

Network heavy Family Office investors have also been more hesitant to make a move back, although perhaps for different reasons to CVCs. Family Offices are patient capital and also look for capital preservation – as they are under little pressure to invest capital they can afford to hold back. It also points to their investment style, where founders and management teams are met and the ‘idea’ of the business is heavily relatable or is a life-long passion of the investor.

Absolute financing methods have jumped into virtual ways of working with two feet

On the other side of the pond, there is a clear leader in confidence in Venture Debt players – in fact 86% of investors (Very and Mostly) are ready for these ways of working to continue. The most financially driven source of venture funding, with no loss of equity or independence, will often heavily focus their diligence on the metrics of companies they invest in. As a result, there is no reason why this cannot be done without meeting the actual management of the business – they are able to obtain comfort through looking at historical data and well backed up assumptions of future forecasts.

It was interesting to note that VCs and VCT / EIS funds had almost identical results, despite the fact that the return profile of these two are vastly different. This is perhaps pointing to the fact that the mechanism behind how both sets of funds work is broadly the same – they are all investing other people’s money and are judged / commissioned on their performance as a result. The level of involvement in their investments are similar too, taking a board seat position and looking to open doors for the businesses to scale.

Overall though the majority of VCs (55% – very and mostly) and VCT / EIS funds (54% – very and mostly) do have the confidence levels to continue activity levels by completely virtual deals.

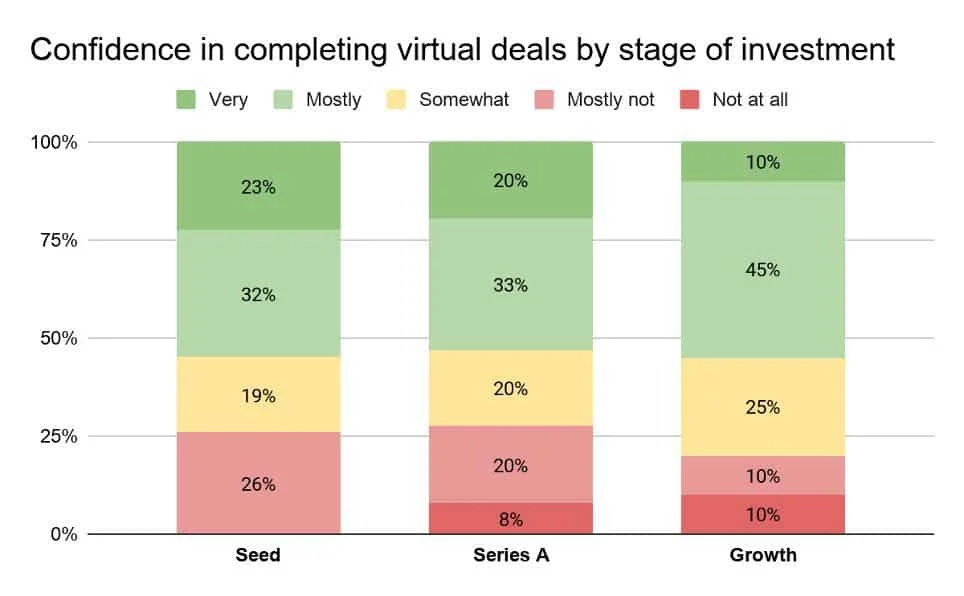

Which about by the stage of investment? How does this look?

With such a wide range of feelings between the types of investor, it has been really intriguing to see a much more consistent response level across the stages of investment. For the purposes of this analysis the following investment stages have been used; Seed (£0.1m – £1m), Series A (£1m – £10m), Growth (£10m+).

It can therefore be concluded that the attitude towards adjusting towards a more virtual strategy will be broadly consistent, no matter the stage of investment, albeit the first movers will likely come at the lower end tickets. Growth deals have fallen much more than seed and series A since COVID-19 – the reason being bigger check sizes and growth capital can be used for international expansion and new product lines, which can defer in a crisis.

What next for Venture?

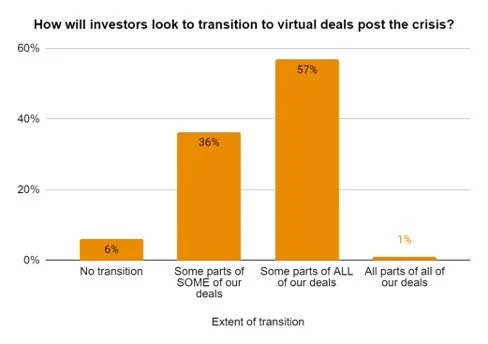

With 94% of venture investors looking to virtually transition at least some parts of their ways of working going forward, the investment scene is starting to establish some new working practices.

With 94% of venture investors looking to virtually transition at least some parts of their ways of working going forward, the investment scene is starting to establish some new working practices.

It is evident from the analysis that the more financially centric an investment, the more likely it is to a) be done virtually currently and b) continuing performing deals this way in the future.

For deals that require more strategic alignment, it will be a lot harder to get noticed and without warm introductions or prior knowledge of the business, they will be challenging to reach.

However, in the long run I believe the impact of the lockdown will be positive on venture. Newer, perhaps more modern, ways of working are being established. Virtual stages are being integrated across the board and this will mean more efficient access to capital – capital that is not restricted by networks or geography.