Oxford and Cambridge are fertile breeding grounds for university spinouts, producing more than 359 companies from 2011 to January this year – taking first and second place across the UK, according to Beauhurst.

These spinouts have contributed significantly to the UK’s economy, climate change efforts, and pushed boundaries in fields ranging from biotechnology and quantum computing to AI and clean energy.

Who comes out on top? It depends on the metric. For spinout creation, the University of Oxford remains the leading institution, producing 210 between 2011 and January 2024, versus 149 for the University of Cambridge.

But while spinouts from the University of Oxford receive pre-money valuations that are on average £4m higher than their University of Cambridge counterparts, they are 2.5 times more likely to go bust, according to data compiled by accounting firm Price Bailey.

But Dominic Vergine, CEO and Founder, Monumo, believes “One thing that I believe is critical to much of the innovation in Cambridge is the university’s spinout structure. The university has always taken a more founder-friendly approach to the university’s equity stake in a spinout, making it easier to create a commercial business that can grow. If this was to ever change, I’m sure we would see a dip in the number of successful Cambridge startups.”

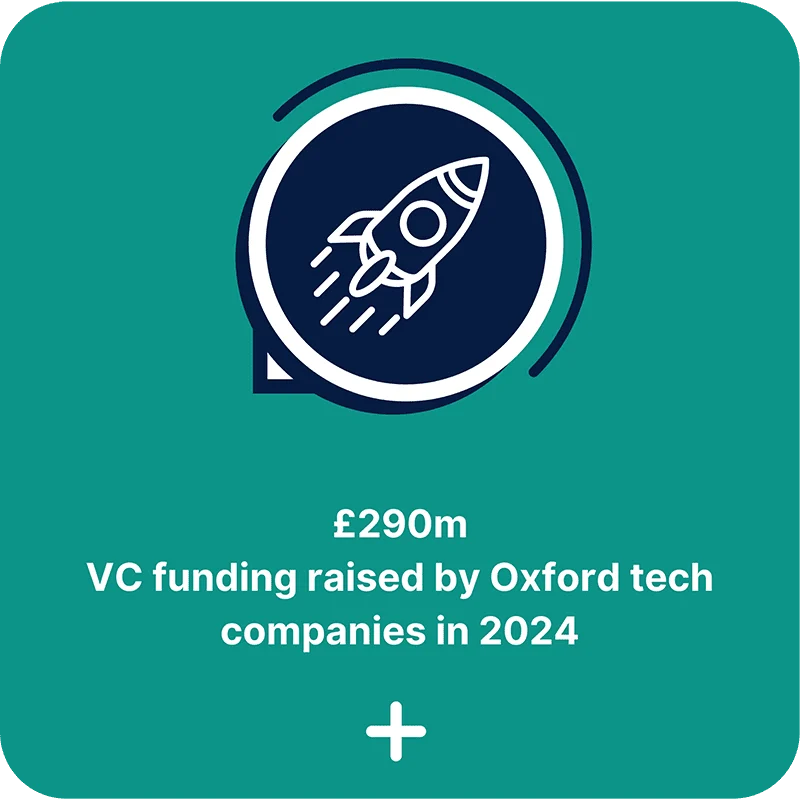

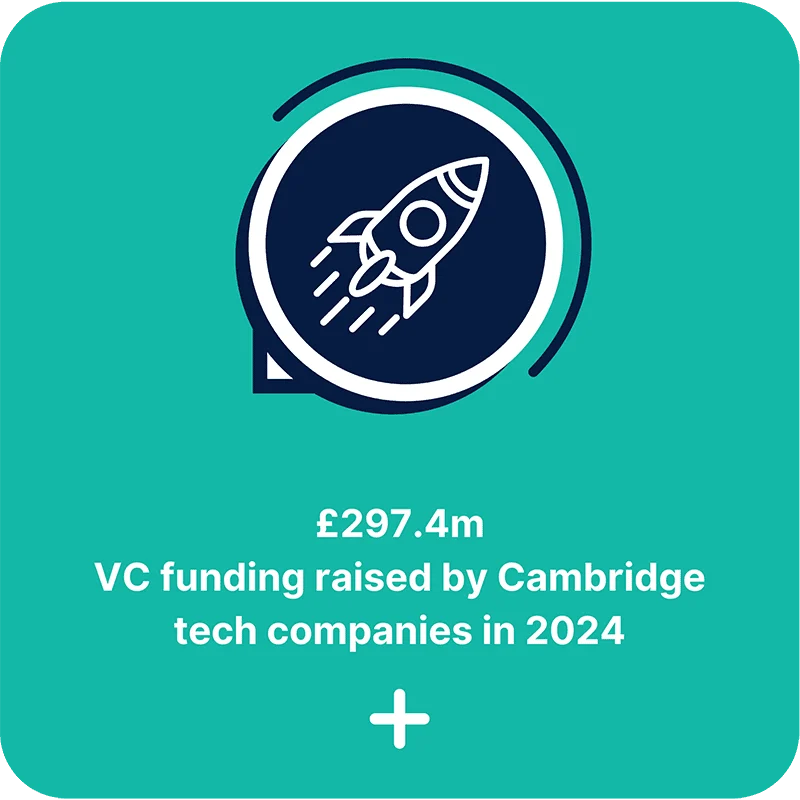

Combined, Oxford and Cambridge spinouts have raised more than £7bn since 2011. This includes Biomodal, an engineering biology company focused on developing genome sequencing technologies. It has raised a total of £106m in equity since it launched in 2014.

Other notable spinouts include Vaccitech, the Oxford-based startup behind the technology used in the AstraZeneca Covid-19 vaccine, and Cambridge Quantum Computing, now Quantinuum, which has become a global leader in quantum software and quantum cybersecurity.

Oxford and Cambridge spinouts have gone on to generate significant returns for investors, tech transfer offices and founders. University of Oxford spinout Onfido, which has created software to verify customer identities, was acquired by US payments firm Entrust in 2024. It was the university’s largest-ever return on investment for a student-led startup. Meanwhile, Oxford Nanopore Technologies, 2021 IPO raised gross proceeds of £428m.